The second day of IFFO’s 2026 Members Meeting in Madrid (29 April 2026) explored the use of marine ingredients in animal farming, human health, and growing sustainability demands in feed.

Salmon markets shift focus to Asia

Starting with the industry often in the spotlight, that of salmon farming, Carl-Emil Kjølås Johannessen from Pareto Securities presented the complexities facing investors and producers, from the impacts of tariffs, biological challenges and the emergence of new technologies. As seafood continues to outperform other animal proteins, the salmon market has grown 3.8% per year since 2006 and seafood in general has grown 2.4% annually, both outperforming other animal proteins with 1.9% annual growth. Carl-Emil noted that “while demand in the US and European markets has slowed since 2002, it is growing in Asia, most notably China, where at this pace they are set to consume 1/10 kilo of salmon produced globally in 2030”.

Starting with the industry often in the spotlight, that of salmon farming, Carl-Emil Kjølås Johannessen from Pareto Securities presented the complexities facing investors and producers, from the impacts of tariffs, biological challenges and the emergence of new technologies. As seafood continues to outperform other animal proteins, the salmon market has grown 3.8% per year since 2006 and seafood in general has grown 2.4% annually, both outperforming other animal proteins with 1.9% annual growth. Carl-Emil noted that “while demand in the US and European markets has slowed since 2002, it is growing in Asia, most notably China, where at this pace they are set to consume 1/10 kilo of salmon produced globally in 2030”.

In regards to how the industry is adapting to challenges, Carl-Emil presented the array of new technologies that are coming online, from a more diverse range of farming types, such as land based, submergible, semi closed and offshore, with systems being adapted to each setting. He added that there remains a high level of interest from investors, and the trend of consolidation among salmon farmers continues globally.

Growth in fed aquaculture continues despite global disruption

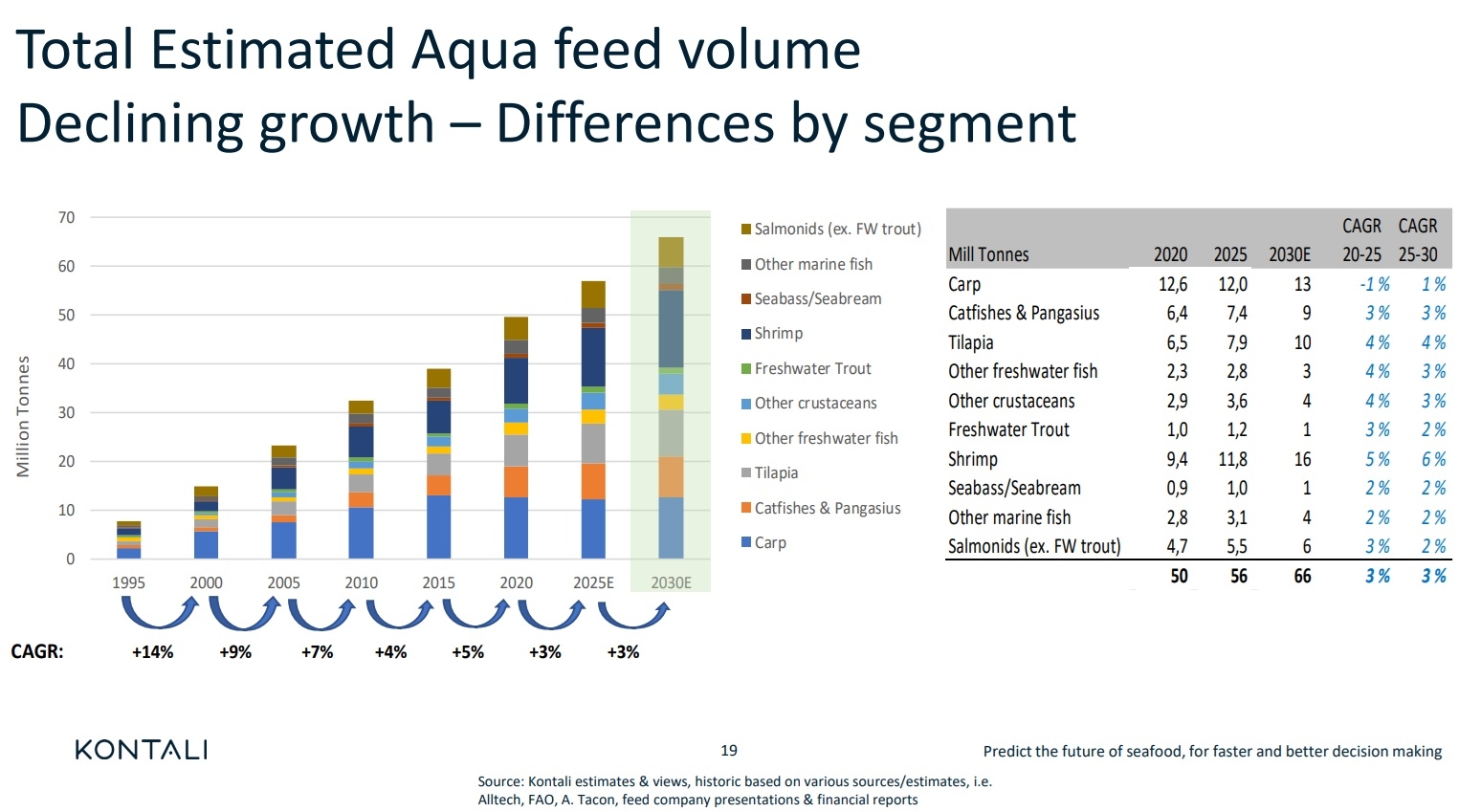

Moving to wider fed aquaculture, Ragnar Nystøyl from Kontali summarised the major and recent trends, while still keeping track of the long lines in aquaculture. Nystøyl stated that “fed aquaculture is still experiencing growth, albeit at a lower growth rate then seen be over the past years”. When highlighting key areas of growth, Nystøyl noted that Ecuador is spearheading the volume-growth in Vannamei shrimp aquaculture and farmed Atlantic salmon, which has seen rebounding growth in 2025, driven by productivity-gains and high sea-temperatures.

Moving to wider fed aquaculture, Ragnar Nystøyl from Kontali summarised the major and recent trends, while still keeping track of the long lines in aquaculture. Nystøyl stated that “fed aquaculture is still experiencing growth, albeit at a lower growth rate then seen be over the past years”. When highlighting key areas of growth, Nystøyl noted that Ecuador is spearheading the volume-growth in Vannamei shrimp aquaculture and farmed Atlantic salmon, which has seen rebounding growth in 2025, driven by productivity-gains and high sea-temperatures.

On tariffs, Nystøyl added that they have had varying impacts on the industry, shifting export streams, and adding new obstacles. Warmwater shrimp, farmed salmon, tilapia and catfish are all to some degree important in the US market, and with import tariffs ranging from notable to destructive, it has caused impacts on trade flows, market distribution and on production. Nystøyl concluded by saying that the fed aquaculture market will prevail as there will still be demand, but with global political instability causing logistical challenges and disruption, costs and complications will be expected across the value chains.

Blended oils, sustainability and risks

Providing insights from a feed producer's perspective, Skretting’s Jorge Diaz Salinas introduced the benefits and challenges of using blended oils in aquaculture. Diaz noted that while they provide a great solution to fulfilling the nutritional requirements of the fish in times of scarcity, they do present challenges in ensuring that these mixed are both traceable and from sustainable sources. Fish oils are blended with vegetable oils to meet market cost demands as the price of fish oils alone has been too high, but the lack of transparency has driven the use of non-certified fish oils and incorrect reporting.

Providing insights from a feed producer's perspective, Skretting’s Jorge Diaz Salinas introduced the benefits and challenges of using blended oils in aquaculture. Diaz noted that while they provide a great solution to fulfilling the nutritional requirements of the fish in times of scarcity, they do present challenges in ensuring that these mixed are both traceable and from sustainable sources. Fish oils are blended with vegetable oils to meet market cost demands as the price of fish oils alone has been too high, but the lack of transparency has driven the use of non-certified fish oils and incorrect reporting.

“Traceability is essential for responsible marine oil sourcing. When we don’t report the use of marine ingredients on the blended oils, we don’t really know what we’re using in the feed and therefore there’s a big risk – an unnecessary risk- for everyone in the value chain.”, Diaz summarised. He added that Skretting’s goal is to protect sustainability integrity and ensure that responsible suppliers are not at disadvantage due to malpractices, if a product cannot be traced that it cannot be verified.

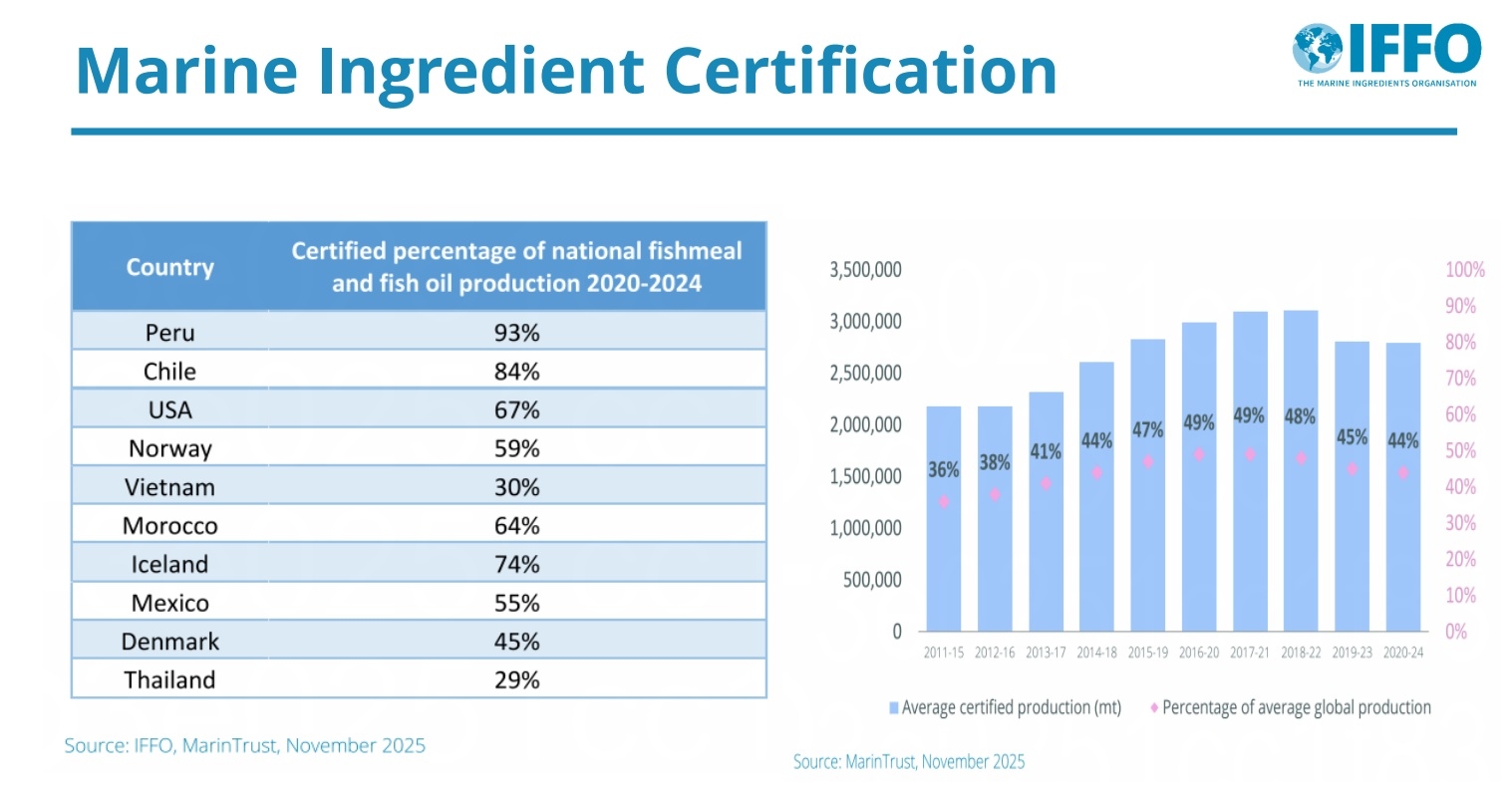

Blending often involves multiple inputs, multiple handovers, and transformation steps that make it easier for information on origin, certification status, and quantities to become blurred or lost. MarinTrust’s Chain of Custody Standard is exploring providing additional assurances on blended oils, which is welcome. The Chain of Custody ensures that the integrity of MarinTrust certified marine ingredients are maintained throughout the supply chain. “Certification standards are the best tools we have. There needs to be alignment across seafood standards on their auditing requirements for blended oils, and these need to be adopted across the value chain”.

Consistent growth in China

Moving to the growing Chinese market, IFFO’s China Director Maggie Xu explained that government authorities continue to optimize market access control policies to increase accuracy and flexibility. Xu added that fishmeal and fish oil imports by China reached an all-time high in 2025, when the thin profit margins triggered a year-over-year contraction in domestic production. Fish oil exports for feed purposes have decreased in the last year, mainly from domestic crude fish oil, but they are expected to increase in response to constraints in global crude fish oil supply. Last year, China’s fishmeal and fish oil consumption sustained the elevated levels of 2024 while this year is expected to see a contraction. Regarding marine catches, they are slightly higher than in 2024, but less wild captures were used in marine ingredients production in 2025 in response to the new fishing law which promotes sustainability.

Moving to the growing Chinese market, IFFO’s China Director Maggie Xu explained that government authorities continue to optimize market access control policies to increase accuracy and flexibility. Xu added that fishmeal and fish oil imports by China reached an all-time high in 2025, when the thin profit margins triggered a year-over-year contraction in domestic production. Fish oil exports for feed purposes have decreased in the last year, mainly from domestic crude fish oil, but they are expected to increase in response to constraints in global crude fish oil supply. Last year, China’s fishmeal and fish oil consumption sustained the elevated levels of 2024 while this year is expected to see a contraction. Regarding marine catches, they are slightly higher than in 2024, but less wild captures were used in marine ingredients production in 2025 in response to the new fishing law which promotes sustainability.

For fish oil for direct human consumption, Xu noted that reduced global supply will result in shrinking exports because Chinese refiners only accept premium and imported crude fish oil. Fish oil consumption is becoming increasing popular with as China’s aging population focuses on health, fish oil is also increasingly sought after by Chinese pet owners.

Panel: Feed producers’ 2030 sustainability targets in practice

A panel discussion chaired by IFFO’s Brett Glencross brought together Rúni Weihe of Havsbrún, Jorge Diaz Salinas of Skretting, and Michiel Fransen from the Aquaculture Stewardship Council (ASC) to explore the role, performance and sustainability of marine and alternative feed ingredients in aquaculture.

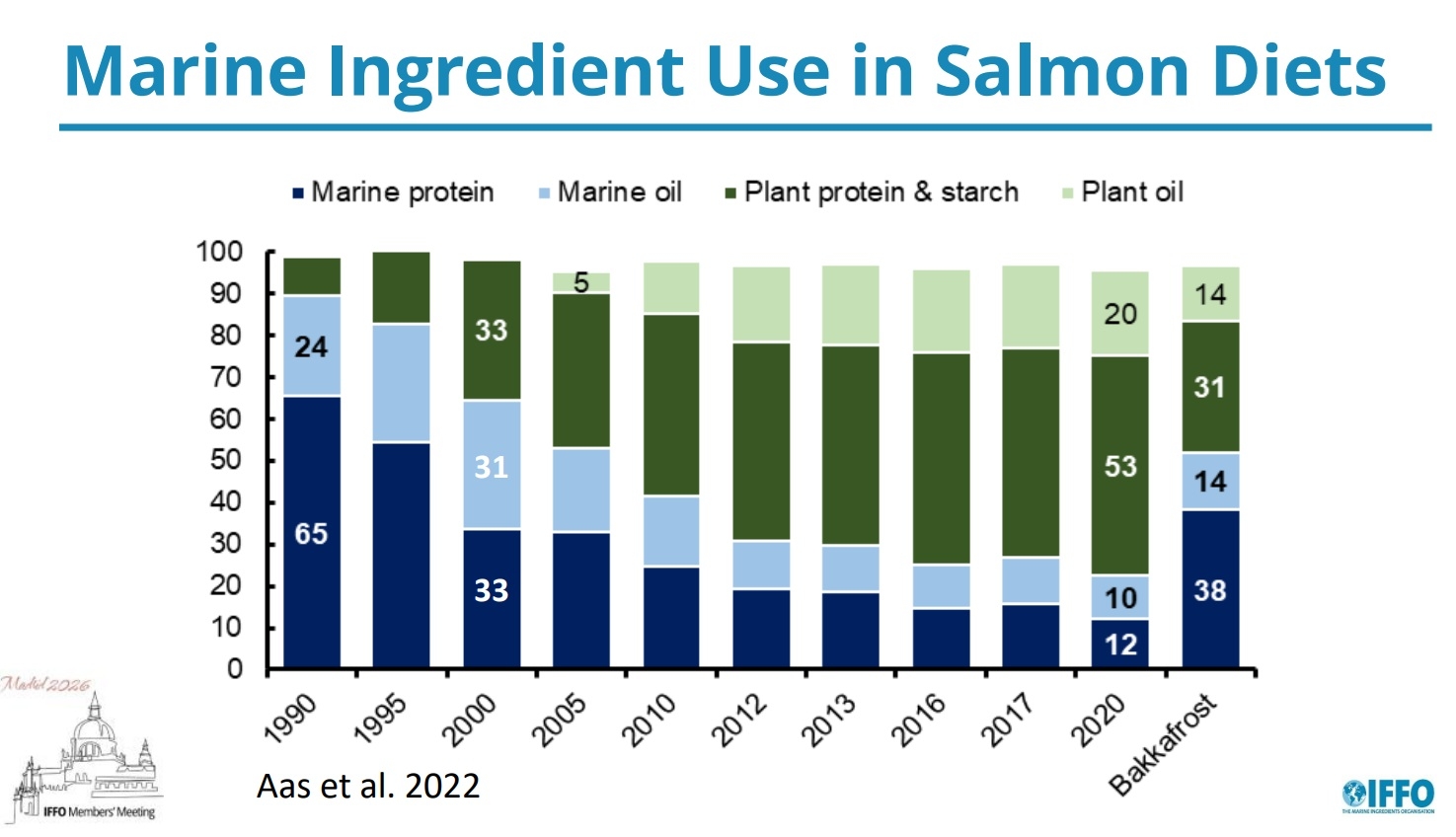

Havsbrún, a Faroe Islands‑based producer of fishmeal, fish oil and high‑quality compound feeds, is a subsidiary of salmon farming company Bakkafrost. Rúni Weihe explained that Bakkafrost’s salmon feed currently contains 38% marine protein and 14% marine oil, complemented by 31% plant protein and starch and 14% plant oil. According to Weihe, trials using higher levels of plant ingredients have not produced equivalent results, reinforcing Havsbrún’s confidence that marine ingredients remain the most effective feed components.

Jorge Diaz Salinas acknowledged that marine ingredients are the preferred option, provided they are responsibly sourced, but warned that availability is limited. Marine ingredients alone will not be sufficient to meet future demand, and their reduced availability creates pressure to use alternatives, which often come at a higher cost. He stressed the need to understand trade‑offs and to ensure flexibility in sourcing, particularly in the context of geopolitical tensions. Referring to Norway’s ambition to increase the share of domestically produced feed raw materials from 8% to 25% by 2034, Diaz Salinas emphasised that feed producers must have access to the right ingredients at the right time and price, without becoming overly dependent on specific regions.

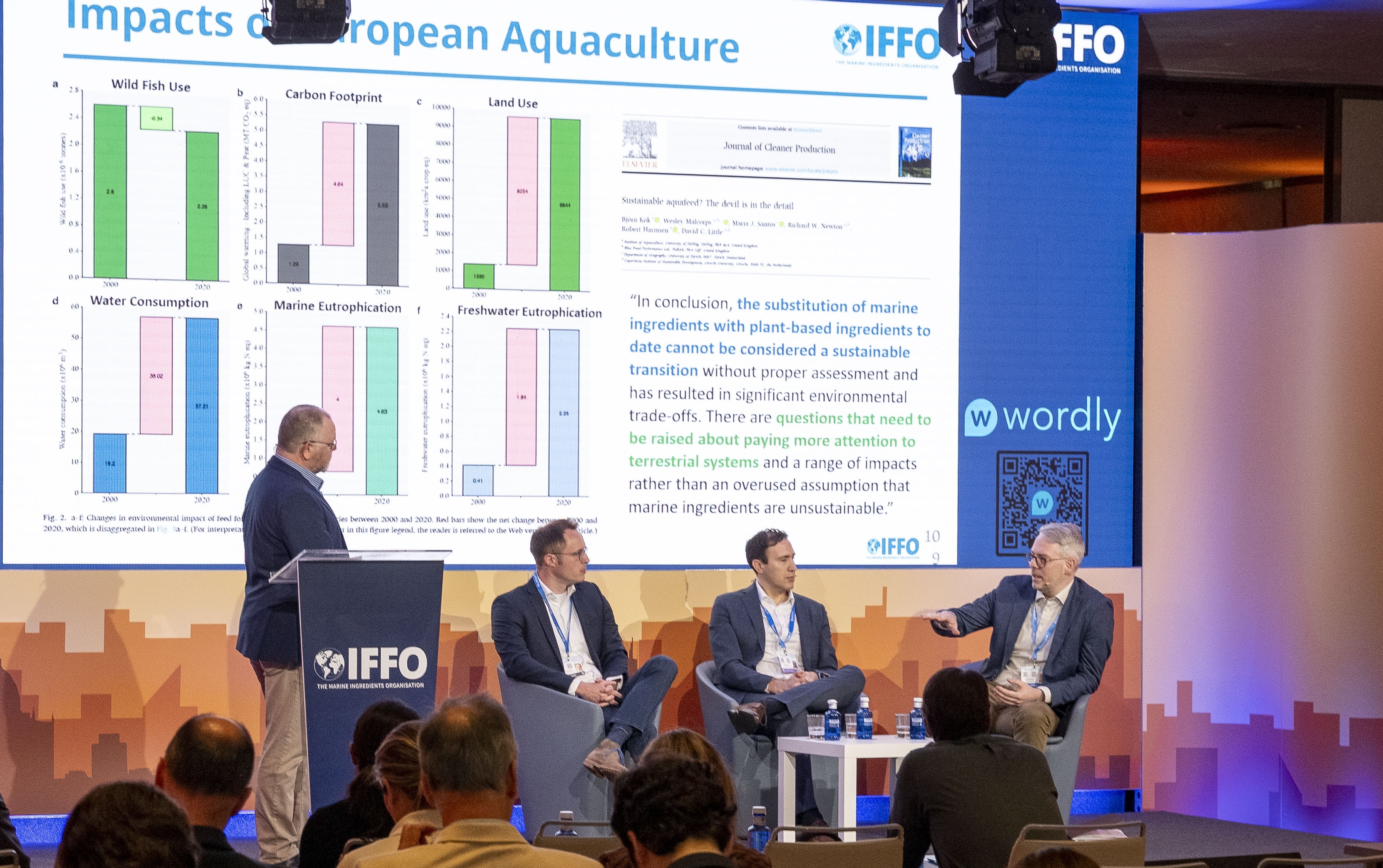

Michiel Fransen highlighted that while marine ingredients often attract the most scrutiny, plant‑based alternatives also present significant challenges. ASC continues to have concerns around plant ingredients, including issues related to deforestation, eutrophication and broader environmental impacts. He noted that the carbon footprint of many terrestrial ingredients is higher than that of marine ingredients, and that sustainability assessments need to consider the full picture. The marine ingredients sector, he argued, is increasingly supported by scientific evidence and is one of the few commodities where clear progress is being made, driven by initiatives such as MarinTrust.

Fransen further explained that ASC aims to provide transparency across the supply chain. All reports on certified feed mills and feed farms are publicly available on the ASC website without password protection. However, he observed that positive developments within the marine ingredients sector are not reaching markets or consumers. In this information vacuum, outdated or poor practices continue to dominate online narratives. This places ASC in a difficult position between industry and markets and highlights the need to better educate retailers and consumers.

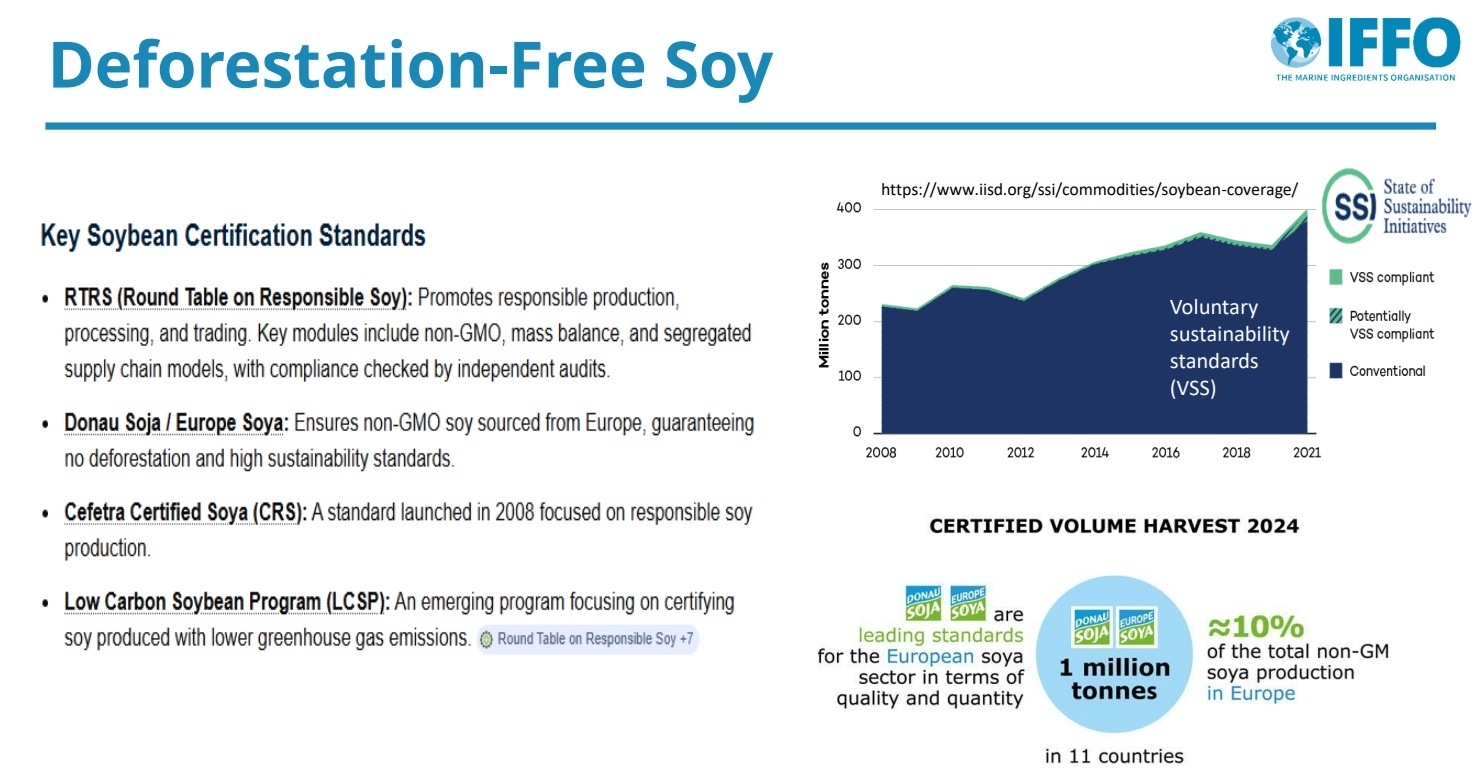

The panel agreed that sustainability should not be framed as a choice between marine or plant ingredients. Instead, it must be an “and, and, and” approach, recognising that all ingredients are needed. Fransen referred to the University of Stirling study “Sustainable feed: the devil is in the detail”, which underlines the importance of nuanced assessment rather than simplistic targets. He also noted that metrics such as FI:FO and FFDR were originally driven by NGO pressure, yet similar scrutiny is often absent in other commodity sectors, such as soy.

Discussion also touched on by‑products. Weihe pointed out that by‑product utilisation is embedded in whole‑fish processing. Without fishmeal production, valuable nutrients would not be recovered and made available to the food system. Skretting confirmed that it continues to increase its use of by‑products, while managing variability in raw material composition to meet fish nutritional requirements.

Brett Glencross noted that the eFIFO for Atlantic salmon fell below 1 in 2020, prompting discussion on whether the industry should move beyond FIFO metrics towards a broader food‑in, food‑out approach that incorporates all feed ingredients.

The panel broadly agreed that sustainability frameworks must evolve alongside the realities of ingredient availability, performance, and environmental impact.

The discussion concluded with a shared message: marine ingredients remain essential, availability is naturally constrained, and progress depends on responsible sourcing, transparency, and a balanced understanding of trade‑offs across all feed ingredients.

Growth in circular and alternatives oils

Looking at global fish oil market production and consumption trends, Jorge Garcia from Marex Global Sourcing provided analysis on Peru’s production, noting that so far landings are below expectations, with high juvenile presence and lower oil yield. Garcia explored the growth potential of circular oils, in areas such as the Chilean salmon industry and the continuing growth of in demand for alternative oils. Garcia concluded that while challenges remain ahead, we are seeing growth with limited supply and increasing resilience to specific origin shortages, these will be tested further with the trade and logistical challenges that lie ahead.

Looking at global fish oil market production and consumption trends, Jorge Garcia from Marex Global Sourcing provided analysis on Peru’s production, noting that so far landings are below expectations, with high juvenile presence and lower oil yield. Garcia explored the growth potential of circular oils, in areas such as the Chilean salmon industry and the continuing growth of in demand for alternative oils. Garcia concluded that while challenges remain ahead, we are seeing growth with limited supply and increasing resilience to specific origin shortages, these will be tested further with the trade and logistical challenges that lie ahead.

Further refining of oils to ensure supply

Moving even more in-depth to the Omega-3 Ingredient Market, GOED’s Aldo Bernasconi, opened by stating that the global EPA and DHA omega-3 industry continues to be a diverse, thriving market with global reach and a variety of sources feeding into a robust category backed by solid science. Bernasconi provided an updated view of the size of the demand for omega-3 ingredient oils, and a summary of relevant current trends, challenges and opportunities. While the omega-3 industry is extremely reliant on anchoveta, which creates risk when there are inevitable supply disruptions, there is now increased reliance on other (new and existing) sources and production of concentrates, which is more efficient. Bernasconi added that traditional 18/12 refined oils are being replaced by refined oils with a total of 30% omega-3, with less specific EPA to DHA ratios and this allows the industry some necessary flexibility.

Moving even more in-depth to the Omega-3 Ingredient Market, GOED’s Aldo Bernasconi, opened by stating that the global EPA and DHA omega-3 industry continues to be a diverse, thriving market with global reach and a variety of sources feeding into a robust category backed by solid science. Bernasconi provided an updated view of the size of the demand for omega-3 ingredient oils, and a summary of relevant current trends, challenges and opportunities. While the omega-3 industry is extremely reliant on anchoveta, which creates risk when there are inevitable supply disruptions, there is now increased reliance on other (new and existing) sources and production of concentrates, which is more efficient. Bernasconi added that traditional 18/12 refined oils are being replaced by refined oils with a total of 30% omega-3, with less specific EPA to DHA ratios and this allows the industry some necessary flexibility.

Regarding conflict in the Middle East, Bernasconi noted that this has resulted disruptions in shipping and increased fuel prices, and further inflation is now likely. Consumer confidence in Europe and the US remains low, so there may be changes in demand of dietary supplements or (less likely) pet nutrition products. While demand for omega-3 pharmaceuticals has been relatively stable, trade in Europe has been slowed by regulatory and reimbursement approval in each country. While in China, the decision on reimbursement is still pending and the government is also taking measures to restrict the types of supplements sold to protect the pharma market.

Reaction to crude oil price spikes

The last presentation was by Adam Ismail from KD Pharma Group , who explored how the omega‑3 industry navigated the recent crude fish oil shortage. Ismail highlighted the diverse strategies companies employed, from reallocating inventory and adjusting formulations to accelerating the shift toward higher‑concentrate, algae‑based, and alternative omega‑3 sources.

The last presentation was by Adam Ismail from KD Pharma Group , who explored how the omega‑3 industry navigated the recent crude fish oil shortage. Ismail highlighted the diverse strategies companies employed, from reallocating inventory and adjusting formulations to accelerating the shift toward higher‑concentrate, algae‑based, and alternative omega‑3 sources.

Looking at the broader market consequences of the 2024 crude oil price spike, Ismail noted that this created significant inflationary pressure across the value chain and, according to consumption data, erased years of progress in increasing global omega‑3 intake. Together, these dynamics offer important lessons on resilience, supply‑chain fragility, and how short‑term supply shocks can reshape long‑term demand, pricing power, and consumer access in the omega‑3 sector. He added that the industry's dependence on a single Peruvian anchovy fishery created systemic risk; and algae, by-product marine oils, other fisheries and plant omega-3 sources are strategic hedges and not niche plays.