This year’s IFFO China Summit was held in Shanghai from 10th-11th June and once again broke records with 221 attending from 27 countries and regions. Discussions at the summit covered global supply and demand, market developments across key producing regions (Northern Europe, Chile, Peru, India, Vietnam, China, as well as global perspectives) and certification systems.

Opening the event, Maggie Xu, IFFO’s China Director, stated "We are delighted to welcome the industry back to China for another edition of what has now become an annual event. China continues to play a central role in the global aquaculture sector, both as the world’s largest producer and as a leading user of marine ingredients to support its rapidly developing feed and farming industries. According to OECD-FAO estimates, China is expected to account for 42% of global fishmeal consumption by 2034.”

Opening the event, Maggie Xu, IFFO’s China Director, stated "We are delighted to welcome the industry back to China for another edition of what has now become an annual event. China continues to play a central role in the global aquaculture sector, both as the world’s largest producer and as a leading user of marine ingredients to support its rapidly developing feed and farming industries. According to OECD-FAO estimates, China is expected to account for 42% of global fishmeal consumption by 2034.”

China’s production and consumption continue to soar

Setting the scene with a global market update and deep dive into developments in Asia, IFFO’s Market Research Director, Enrico Bachis noted that global supply of fishmeal and fish oil has remained consistent with average levels seen over the past decade. Asian countries account for roughly 35% of global fishmeal and fish oil production, while intra-regional trade continues to expand. Compared with other regions, pelagic species play a more limited role as raw material for fishmeal and fish oil in Asia, where tuna, tilapia and pangasius represent a relatively larger share.

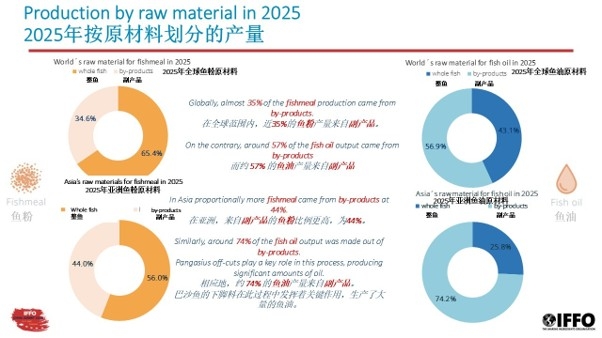

He stated that globally, almost 35% of the fishmeal production came from by-products, and around 57% of the fish oil output came from by-products. In Asia, Bachis added that proportionally more fishmeal came from by-products at 44%, and similarly, around 74% of the fish oil output was made out of by-products. Pangasius off-cuts play a key role in this process, producing significant amounts of oil. Consumption is mainly driven by aquafeed, with crustaceans, freshwater species and marine fish as the main consumers. Bachis concluded by noting that Asia has an annual supply gap of about 1.2 million mt for fishmeal and around 80,000 mt for fish oil used in aquafeed and direct human consumption. Asian countries will continue, for the time being, to rely on imports to meet local marine ingredient demand.

He stated that globally, almost 35% of the fishmeal production came from by-products, and around 57% of the fish oil output came from by-products. In Asia, Bachis added that proportionally more fishmeal came from by-products at 44%, and similarly, around 74% of the fish oil output was made out of by-products. Pangasius off-cuts play a key role in this process, producing significant amounts of oil. Consumption is mainly driven by aquafeed, with crustaceans, freshwater species and marine fish as the main consumers. Bachis concluded by noting that Asia has an annual supply gap of about 1.2 million mt for fishmeal and around 80,000 mt for fish oil used in aquafeed and direct human consumption. Asian countries will continue, for the time being, to rely on imports to meet local marine ingredient demand.

Impacts of El Niño in Peru

Addressing the challenging conditions in Peru, Jorge Risi, General Manager at SNP (Peru’s Sociedad Nacional de Pesquería) presented an update on the world’s leading supplier of marine ingredients, accounting for approximately 8% of global catches and 22% of fishmeal and fish oil production.

Risi summarised that Peru’s anchoveta fishery operates under a strict regulatory framework that includes seasonal quotas, continuous biomass assessments, scientific research cruises, individual vessel catch limits, and precautionary measures to protect juvenile fish and ecosystem sustainability. These measures have contributed to maintaining a healthy biomass and ensuring the long-term viability of the resource. This precautionary approach has meant in response to environmental instability from El Niño has meant that landings this year have fallen markedly. From a market perspective, Peru remains a reliable strategic supplier for China and other international markets. Risi also explored the range of international organizations who recognize the sustainable management of the Peruvian anchoveta fishery, including a recent OECD report (March 2026). “The future competitiveness of Peruvian marine ingredients relies on the responsible management of its fisheries, which is based solely on scientific evidence” Risi said.

Risi summarised that Peru’s anchoveta fishery operates under a strict regulatory framework that includes seasonal quotas, continuous biomass assessments, scientific research cruises, individual vessel catch limits, and precautionary measures to protect juvenile fish and ecosystem sustainability. These measures have contributed to maintaining a healthy biomass and ensuring the long-term viability of the resource. This precautionary approach has meant in response to environmental instability from El Niño has meant that landings this year have fallen markedly. From a market perspective, Peru remains a reliable strategic supplier for China and other international markets. Risi also explored the range of international organizations who recognize the sustainable management of the Peruvian anchoveta fishery, including a recent OECD report (March 2026). “The future competitiveness of Peruvian marine ingredients relies on the responsible management of its fisheries, which is based solely on scientific evidence” Risi said.

Salmon sector drives demand in Chile

Echoing Risi, Francisco Ovalle, Orizon’s Commercial Manager, detailing Chile’s long-term quota system with strong compliance and predictability, ensuring dominance in Jack Mackerel and the world’s second-largest salmon producer. Ovalle noted that while resource fundamentals are broadly healthy, with sustained biomass recovery, particularly in Jack Mackerel, some localized pressures remain in anchovy and sardine fisheries, highlighting the need for continued adaptive management. “In spite of the various environmental challenges, Chile has managed to catch an average of 80% of the granted quotas over the last decade. The Chilean industry remains resilient”.

Echoing Risi, Francisco Ovalle, Orizon’s Commercial Manager, detailing Chile’s long-term quota system with strong compliance and predictability, ensuring dominance in Jack Mackerel and the world’s second-largest salmon producer. Ovalle noted that while resource fundamentals are broadly healthy, with sustained biomass recovery, particularly in Jack Mackerel, some localized pressures remain in anchovy and sardine fisheries, highlighting the need for continued adaptive management. “In spite of the various environmental challenges, Chile has managed to catch an average of 80% of the granted quotas over the last decade. The Chilean industry remains resilient”.

Looking ahead, the sector’s outlook remains positive, but exposed to environmental volatility, particularly the expected El Niño cycle, which could affect their key species. Ovalle added that Chile’s fishing sector is evolving towards higher-value utilization, with a growing share of catches directed to direct human consumption rather than reduction into fishmeal and fish oil. He added that the fishmeal and fish oil markets are mature and export-oriented, with China as the dominant customer representing 49,1% of the fishmeal exports, and with domestic fishmeal increasingly influenced by strong demand from the salmon aquaculture industry. He concluded saying “this salmon sector acts as the primary demand engine, driving steady growth in feed production and long-term consumption of marine ingredients.”

European certification demands moving markets

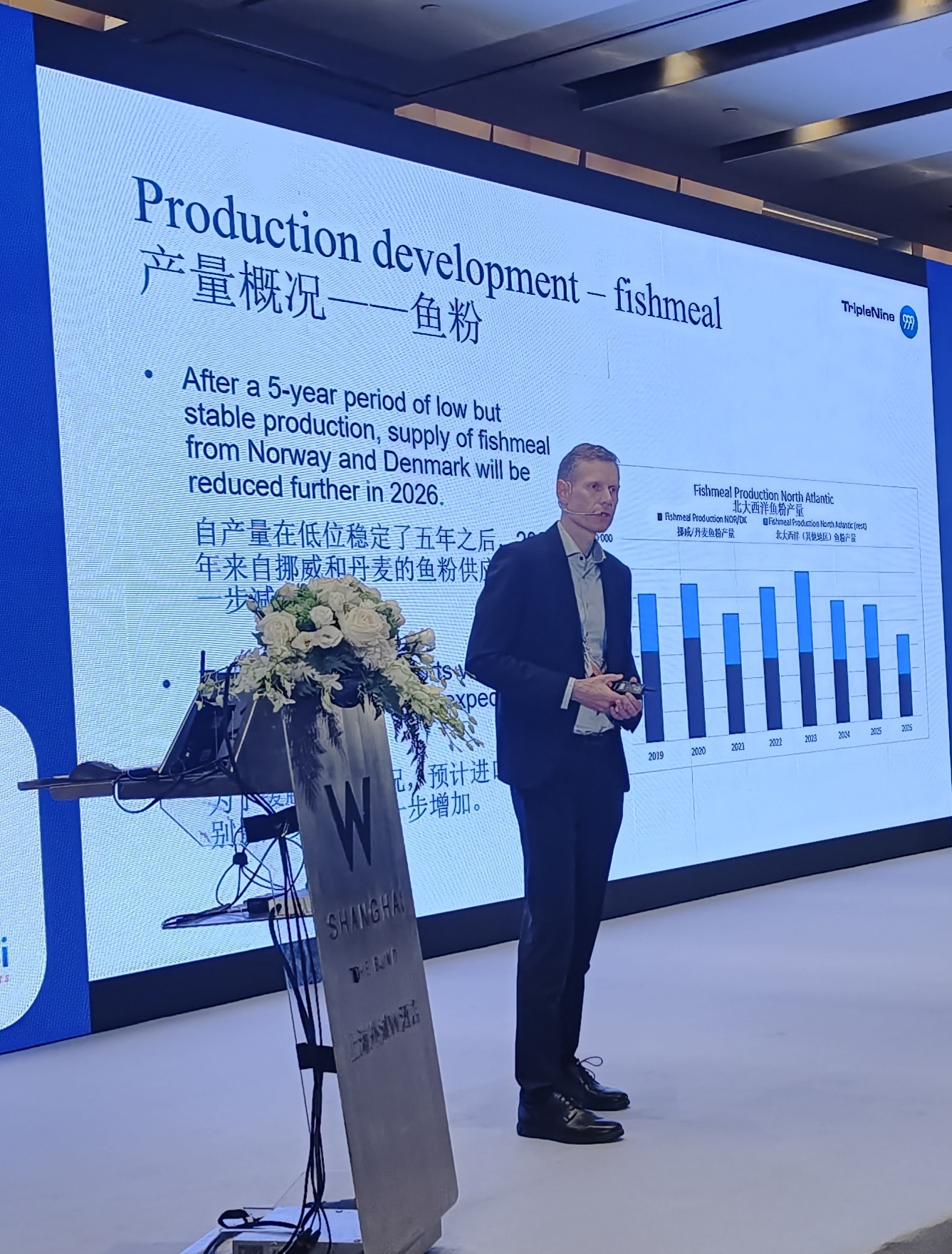

Moving to Europe, TripleNine’s Chief of Sales and Operations, Kenneth Storbank presented an update on production in Denmark and Norway. In Europe, Storbank noted that the main consumer of fishmeal and oil remains the salmon segment, which continues to grow, increasing demand and thereby reducing export as Europe is now depending on import of both fishmeal and oil to fulfil the demand. While numerous whole fish species are used for fishmeal and fish oil in Europe, Blue Whiting is by far the most important species for fishmeal production, with other species and trimmings dominating fish oil production, with a third of all raw material received as trimmings.

Moving to Europe, TripleNine’s Chief of Sales and Operations, Kenneth Storbank presented an update on production in Denmark and Norway. In Europe, Storbank noted that the main consumer of fishmeal and oil remains the salmon segment, which continues to grow, increasing demand and thereby reducing export as Europe is now depending on import of both fishmeal and oil to fulfil the demand. While numerous whole fish species are used for fishmeal and fish oil in Europe, Blue Whiting is by far the most important species for fishmeal production, with other species and trimmings dominating fish oil production, with a third of all raw material received as trimmings.

Quota sizes of these short-lived species variate strongly from year to year depending on especially recruitment success. Storbank added that a declining spawning-stock biomass has led to a significant reduction in quota this year, a trend that may continue in 2027. He added coastal sharing agreements have failed since 2018, resulting in higher fishing pressure than ICES’ scientific advice, and enrolment in a Fishery Improvement Project (FIP), which will end in October 2026. “It is much easier for European producers to deliver marine ingredients to European customers, but from 2027 our presence in Asia will grow due to a change in the market fundamentals” explained Storbank.

Growth continues in India

Providing insights from India’s marine ingredients industry, John Joseph from Arbee summarised that the country has seen a steady recovery in marine landings, with the return of stable oil sardine biomass, and the lifting of long-standing regulatory restrictions on new fishmeal and fish oil plants. India is now among the top three global producers of fish, with marine landings of 3.57 million tons in 2025 and total fish production of nearly 17 million tons including aquaculture, shipping to over 130 countries, with China and Vietnam as leading consumers of fishmeal. “The relationship with China moved from an opportunistic short-term rapport to a solid long-standing partnership, adding a stable flow of fishmeal into the biggest market in the world” Joseph explained. Joseph added that Pelagic finfish continues to dominate the catch composition, with the utilization of trimmings from seafood canning units (sardines, mackerel, tuna, pink perch) increasing as a critical secondary feedstock. Joseph mention efforts to improve continue, with existing Fishery Improvement Projects, in Karnataka, Maharashtra and Goa, with more starting up. Looking ahead Joseph added that this year’s monsoon is forecast normal-to-above-normal, with landing forecasts are optimistic and fishing bans remaining the same

In terms of domestic consumption of marine ingredients, Joseph noted that India Omega-3 supplements market projected to reach to grow at a CAGR of 10.9%. More than 50% of demand is still met by Chinese concentrates and European finished products, but this share is shrinking as domestic refining scales up. He added that pet nutrition is the fastest-growing application segment for fish oil in India, alongside omega-3 refining for human nutrition, and ahead of aquafeed in growth rate.

Strong cooperation ensures growth in Vietnam

Covering Vietnam, Kanematsu’s Ngo Nha Truc noted that there is increasing demand for high-quality aquafeed driven by shrimp, pangasius and marine fish farming, with aquafeed now accounting for 5% of total feed production. This shows the continued importance of marine ingredients, especially fishmeal, in supporting feed performance, digestibility and farming efficiency. He added however that domestic supply remains under pressure, with fishmeal production only operating at around 60-70%, mainly due to raw material shortages, seasonality and inconsistent quality. Nha Truc added that use of seafood processing by-products is growing and now contributes approximately 40–60% of raw material supply, but local production is still insufficient to meet growing demand. “Despite the significant domestic production of marine ingredients, Vietnam remains heavily dependent on imported marine ingredients for premium aquafeed production” Truc argued. For China, Nha Truc noted that Vietnam represents both a neighbouring aquaculture hub and an important participant in regional marine ingredient supply chains. Both markets are exposed to global fishmeal price volatility, sustainability requirements and competition for high-quality raw materials. She concluded by saying that “stronger cooperation between Vietnam and China in sourcing, quality standards and by-product utilisation will therefore be important for long-term supply resilience.”

Covering Vietnam, Kanematsu’s Ngo Nha Truc noted that there is increasing demand for high-quality aquafeed driven by shrimp, pangasius and marine fish farming, with aquafeed now accounting for 5% of total feed production. This shows the continued importance of marine ingredients, especially fishmeal, in supporting feed performance, digestibility and farming efficiency. He added however that domestic supply remains under pressure, with fishmeal production only operating at around 60-70%, mainly due to raw material shortages, seasonality and inconsistent quality. Nha Truc added that use of seafood processing by-products is growing and now contributes approximately 40–60% of raw material supply, but local production is still insufficient to meet growing demand. “Despite the significant domestic production of marine ingredients, Vietnam remains heavily dependent on imported marine ingredients for premium aquafeed production” Truc argued. For China, Nha Truc noted that Vietnam represents both a neighbouring aquaculture hub and an important participant in regional marine ingredient supply chains. Both markets are exposed to global fishmeal price volatility, sustainability requirements and competition for high-quality raw materials. She concluded by saying that “stronger cooperation between Vietnam and China in sourcing, quality standards and by-product utilisation will therefore be important for long-term supply resilience.”

Certified marine ingredients are at the heart of aquaculture value chain

MarinTrust’s Impacts Manager, Nicola Clark, provided an overview of the global third-party certification programme, dedicated to responsible sourcing, production and traceability of marine ingredients. With two certification standards, one covering marine ingredient factories and the second ensuring the traceability and integrity of those MarinTrust certified products across the value chain. Clark highlighted the importance of the Standard’s strong pre-requisite sourcing requirements, which ensure both whole and by-products used are aligned to international norms and guidelines, particularly the FAO Code of Conduct for Responsible Fisheries, and avoid IUU fishing activity. She added that growing the use of by-products for marine ingredient production is a key mission for the Factory Standard, as they offer a major opportunity to support circularity, reduce waste, diversify supply and meet market demands. Another key mission is ensuring traceability from source to end product, and MarinTrust plays a central role in advancing global traceability, aligning with the Global Dialogue on Seafood Traceability (GDST) and strengthening social, environmental, and governance requirements in the industry.

As referenced in earlier presentations, MarinTrust also runs an Improver Programme, for those supply chains that require improvement to their raw material sourcing, providing a structured and time-bound process through which marine ingredient production factories sourcing from improving fisheries (FIPs) can gain recognition of their production. Clark concluded that “responsibly sourced marine ingredients remain the most nutritious and digestible aquafeed ingredients, and the largest source of omega-3 fatty acids. MarinTrust sits at the heart of the aquaculture value chain, providing assurances on environmental, social and traceability. We are constantly evolving and responding to market demands and ensuring that certified marine ingredients are recognised and embedded within aquafeed and aquaculture standards. Our recognition of GSSI fisheries standards last year has further improved accessibility and embedding us even further into the wider seafood value chain.”

An Update on the Omega-3 Market

GOED’s VP of Data Science Aldo Bernasconi provided an overview of the global omega3 (EPA/DHA) market, highlighting steady growth, evolving demand, and emerging challenges. He summarised that the finished products market has grown modestly (around 2.5% annually), with the most value concentrated in infant formula and pet nutrition, although infant formula growth is slowing due to declining birth rates, while pet nutrition is expanding rapidly, especially in China.

GOED’s VP of Data Science Aldo Bernasconi provided an overview of the global omega3 (EPA/DHA) market, highlighting steady growth, evolving demand, and emerging challenges. He summarised that the finished products market has grown modestly (around 2.5% annually), with the most value concentrated in infant formula and pet nutrition, although infant formula growth is slowing due to declining birth rates, while pet nutrition is expanding rapidly, especially in China.

Bernasconi stated that demand for omega‑3 ingredient oils continues to increase, growing 3.4% in 2025 and expected to grow about 3.8% annually through 2027. China remains the fastest‑growing and increasingly sophisticated market, alongside rising opportunities in regions like India,

Africa, the Middle East, and Latin America. He added that consumer insights show strong awareness and usage of omega‑3s, particularly in China, where they are consumed from multiple sources and valued for general wellness, as well as brain and heart health benefits. “The demand for petfood that contains omega-3 fatty acids is growing everywhere. In China the growth is staggering” Aldo commented. Finally, Bernasconi concluded that “the industry faces several uncertainties, with limited fish oil supply in 2026, shifts in product formulations, geopolitical and economic disruptions affecting trade and demand, and potential regulatory change, especially in China, where pharmaceutical reimbursement decisions could significantly boost demand.”

China's fishmeal demand is real — but it is not unlimited

Delving into the complexities of China’s fishmeal demand, Zhaogang Jiang, President from Evergreen International Trade (Guangzhou) summarised domestic raw material is tight, with reduced domestic fishmeal production in 2025, and there will be a struggle to fill the import gap. He added that “China isn't a single market, but rather dozens of segmented markets. Eel is one market, shrimp is another, and California bass is yet another. Their fishmeal demand behaviours’ are completely different. Feed companies, caught in the middle, should find a new balance between supply security and cost control.” Jiang concluded noting that while fishmeal demand is unlikely to disappear, it should not be viewed simply as growth either. "The fishmeal demand in China is real, but it is not unlimited and these limits of demand are becoming visible. The pace of response for the local supply will define the real picture of 2026". Chinese feed mills have matured through multiple high-cost cycles, with procurement discipline, safety stock, and delivery risk management so as not to remove fishmeal but using it more precisely. Total demand may remain relatively stable, while fishmeal use per unit of feed is declining.

Delving into the complexities of China’s fishmeal demand, Zhaogang Jiang, President from Evergreen International Trade (Guangzhou) summarised domestic raw material is tight, with reduced domestic fishmeal production in 2025, and there will be a struggle to fill the import gap. He added that “China isn't a single market, but rather dozens of segmented markets. Eel is one market, shrimp is another, and California bass is yet another. Their fishmeal demand behaviours’ are completely different. Feed companies, caught in the middle, should find a new balance between supply security and cost control.” Jiang concluded noting that while fishmeal demand is unlikely to disappear, it should not be viewed simply as growth either. "The fishmeal demand in China is real, but it is not unlimited and these limits of demand are becoming visible. The pace of response for the local supply will define the real picture of 2026". Chinese feed mills have matured through multiple high-cost cycles, with procurement discipline, safety stock, and delivery risk management so as not to remove fishmeal but using it more precisely. Total demand may remain relatively stable, while fishmeal use per unit of feed is declining.